NEW YORK, New York – U.S. stocks closed mixed on Wednesday, despite strong economic data. As expected the Federal Reserve kept interest rates unchanged.

Three major topics greeted markets Wednesday. Firstly came the news that the economy grew more strongly than expected in the second quarter. Then came the announcement by President Donald Trump of a 25 percent tariff being imposed on goods from India, effective August 1. This was followed by the Federal Reserve’s announcement on interest rates.

“Real gross domestic product (GDP) increased at an annual rate of 3.0 percent in the second quarter of 2025, according to the advance estimate released by the U.S. Bureau of Economic Analysis on Wednesday. “In the first quarter, real GDP decreased 0.5 percent.”

The increase in real GDP in the second quarter primarily reflected a decrease in imports.

President Trump in announcing the new tariff on Indian goods, was critical of the southeast Asian country.

“Remember, while India is our friend, we have, over the years, done relatively little business with them because their Tariffs are far too high, among the highest in the World, and they have the most strenuous and obnoxious non-monetary Trade Barriers of any Country,” President Trump wrote on Truth Social.

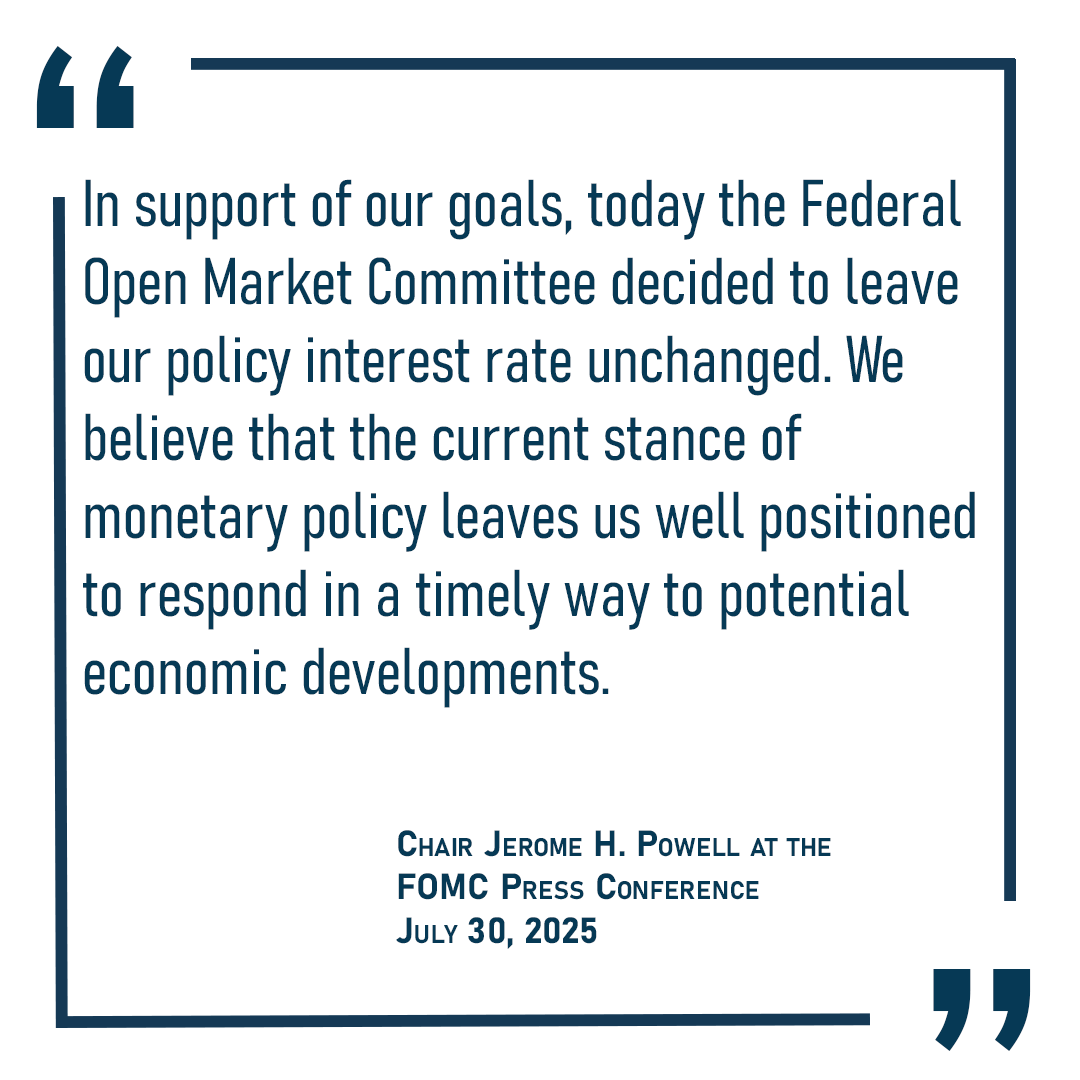

Over at the Federal Reserve the FOMC completed their regular monthly meeting, deciding to leave interest rates unchanged, as expected, and despite President Trump’s call lto lower rates.

“The unemployment rate remains low, and labor market conditions remain solid. Inflation remains somewhat elevated,” the Fed’s committee said in a statement released Wednesday afternoon.

“The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. Uncertainty about the economic outlook remains elevated,” the statement added.

Stocks spent most of the day in the red, but clawed back some ground in the closing minutes of trading, with the tech-heavy Nasdaq Composite bucking the downward trend while blue chips and broader markets retreated.

Key Index Performances

-

S&P 500 (^GSPC): Edged down 7.96 points (0.12 percent) to close at 6,362.90, with trading volume reaching 3.247 billion shares.

-

Dow Jones Industrial Average (^DJI): Fell 171.71 points (0.38 percent) to 44,461.28, marking its third straight day of losses amid weakness in industrial and financial stocks.

-

NASDAQ Composite (^IXIC): Gained 31.38 points (0.15 percent) to finish at 21,129.67, supported by strength in megacap tech names.

The mixed session reflected ongoing investor uncertainty ahead of Friday’s crucial jobs report, with traders weighing strong tech earnings against concerns about slowing economic growth. The NASDAQ’s resilience contrasted with the Dow’s struggles, highlighting the continued divergence between growth and value stocks.

U.S. Dollar Strengthens Against Major Currencies as Euro and Pound Slide

The U.S. dollar gained considerable ground against most major currencies in Wednesday’s foreign exchange session, while the euro and British pound faced significant declines amid shifting economic expectations, following the U.S. GDP rebound, and the Federal Resreve decision to leave official interest rates unchanged.

Key Currency Movements

-

EUR/USD (Euro / US Dollar): Fell sharply by 1.02 percent to 1.1428, marking its weakest level in three weeks.

-

USD/JPY (US Dollar / Japanese Yen): Rose 0.57 percent to 149.30, nearing a key resistance level.

-

USD/CAD (US Dollar / Canadian Dollar): Gained 0.34 percent to 1.3816, supported by weaker oil prices.

-

GBP/USD (British Pound / US Dollar): Dropped 0.74 percent to 1.3243, pressured by soft UK economic data.

-

USD/CHF (US Dollar / Swiss Franc): Surged 0.89 percent to 0.8129, as the Swiss franc lost its safe-haven appeal.

-

AUD/USD (Australian Dollar / US Dollar): Plunged 1.18 percent to 0.6432, its lowest since November 2024.

-

NZD/USD (New Zealand Dollar / US Dollar): Declined 1.04 percent to 0.5893, weighed down by risk-off sentiment.

Market Drivers

The dollar’s rally was fueled by stronger-than-expected U.S. economic data, reinforcing expectations that the Federal Reserve will keep interest rates elevated. Meanwhile, the euro and pound weakened following disappointing Eurozone and UK PMI figures. Commodity-linked currencies, including the Australian and New Zealand dollars, suffered as global growth concerns dampened risk appetite.

Outlook

Traders are now awaiting Friday’s U.S. nonfarm payrolls report for further clues on the Fed’s future policy path. Analysts warn that further dollar strength could extend if the jobs data surprises to the upside.

Global Equity Markets Deliver Mixed Results on Wednesday; Asia and Pacific Indices Show Divergence

Global stock markets closed with mixed performances on Wednesday, as European indices saw modest gains while several Asian and Middle Eastern markets faced declines.

Canadian Markets Finish Lower

The S&P/TSX Composite (^GSPTSE): Canada’s benchmark index dropped 169.92 points (0.62 percent) to 27,369.96, underperforming its U.S. counterparts as energy shares weighed.

Europe Ends Modestly Higher

The FTSE 100 (^FTSE) inched up by 0.62 points to 9,136.94, a marginal gain of 0.01 percent. Germany’s DAX (^GDAXI) climbed 0.19 percent to 24,262.22, while France’s CAC 40 (^FCHI) rose 0.06 percent to 7,861.96. The broader EURO STOXX 50 (^STOXX50E) advanced 0.26 percent to 5,393.18.

However, Belgium’s BEL 20 (^BFX) bucked the trend, slipping 0.13 percent to 4,615.16.

Asia and Pacific Markets Struggle

Hong Kong’s Hang Seng Index (^HSI) tumbled 1.36 percent to 25,176.93, weighed down by tech and property stocks. Singapore’s STI Index (^STI) dipped 0.24 percent to 4,219.41.

Australia’s S&P/ASX 200 (^AXJO) outperformed, rising 0.60 percent to 8,756.40, while the All Ordinaries (^AORD) gained 0.54 percent to 9,015.40.

India’s Sensex (^BSESN) edged up 0.18 percent to 81,481.86, but Indonesia’s IDX Composite (^JKSE) dropped 0.89 percent to 7,549.89. New Zealand’s NZX 50 (^NZ50) fell 0.62 percent to 12,855.97.

Here’s a more comprehensive listing of the key world stock market indices as they closed on Wednesday:

European Markets Edge Higher

-

The UK’s FTSE 100 (^FTSE) inched up by 0.62 points (0.01 percent) to 9,136.94.

-

Germany’s DAX (^GDAXI) climbed 0.19 percent to 24,262.22.

-

France’s CAC 40 (^FCHI) rose 0.06 percent to 7,861.96.

-

The Euro Stoxx 50 (^STOXX50E) gained 0.26 percent to 5,393.18.

-

The Euronext 100 (^N100) advanced 0.20 percent to 1,601.83.

-

Belgium’s BEL 20 (^BFX) dipped 0.13 percent to 4,615.16.

Asia and Pacific Markets Show Volatility

-

Hong Kong’s Hang Seng (^HSI) tumbled 1.36 percent to 25,176.93, dragged by tech and property stocks.

-

Singapore’s STI (^STI) slipped 0.24 percent to 4,219.41.

-

Australia’s S&P/ASX 200 (^AXJO) rose 0.60 percent to 8,756.40, while the All Ordinaries (^AORD) gained 0.54 percent to 9,015.40.

-

India’s Sensex (^BSESN) edged up 0.18 percent to 81,481.86.

-

Indonesia’s IDX Composite (^JKSE) dropped 0.89 percent to 7,549.89.

-

Malaysia’s KLSE (^KLSE) inched up 0.04 percent to 1,524.50.

-

New Zealand’s NZX 50 (^NZ50) fell 0.62 percent to 12,855.97.

-

South Korea’s KOSPI (^KS11) jumped 0.74 percent to 3,254.47.

-

Taiwan’s TWSE (^TWII) surged 1.12 percent to 23,461.72, outperforming the region.

-

China’s Shanghai Composite (000001.SS) rose 0.17 percent to 3,615.72.

-

Japan’s Nikkei 225 (^N225) dipped slightly by 0.05 percent to 40,654.70.

Middle East and Africa See Declines

-

Israel’s TA-125 (^TA125.TA) fell 0.59 percent to 3,086.74.

-

Egypt’s EGX 30 (^CASE30) dropped 0.66 percent to 33,859.70.

-

South Africa’s Top 40 (^JN0U.JO) slipped 0.03 percent to 5,485.90.

Related stories:

Tuesday 29 July 2025 | U.S. stocks retreat ahead of Wednesday’s Federal Reserve meeting | Big News Network

Monday 28 July 2025 | New records set on Wall Street following U.S.-EU trade deal | Big News Network